.webp)

.webp)

Shariah-Compliant Home Financing: A Holistic Look at Islamic Alternatives to Traditional Mortgage

Key Takeaways

- Islamic Financial Ethics: Shariah-compliant home financing avoids interest by using trade-based structures like Murabahah and Tawarruq.

- Market Adaptation: Islamic banks in Malaysia and Singapore offer competitive and ethical financing alternatives.

- Consumer Centric Evolution: Continuous reform and transparency are key to maintaining public trust in Islamic financing products.

Introduction

As Muslim homebuyers increasingly seek ethically aligned and Shariah-compliant options in a fast-expanding property market, Shariah-compliant home financing is emerging as a vital alternative to conventional mortgages. From Malaysia’s prominent Islamic banks to trend-setting developments in Singapore, Islamic home financing is not just a niche product—it’s a financial necessity for many Muslims striving to own homes while staying faithful to their values1.

With growing awareness around interest-free and ethical financial structures, understanding Islamic mortgage offerings helps both Muslim consumers and those curious about Islamic finance navigate the home ownership journey with clarity2.

.webp)

Generalized depiction of rising interest in halal real estate and Islamic mortgage models worldwide

What Is Shariah-Compliant Home Financing?

Shariah-compliant home financing refers to real estate ownership solutions that adhere to Islamic principles. The cornerstone of this model is the prohibition of riba, or interest. Traditional mortgage systems are based on lending money with interest, a practice that is strictly forbidden in Islam.

Instead, Islamic home financing offers alternatives based on trade and sharing of risk, emphasizing justice, fairness (adl), and trust (amanah) between parties.

- Murabahah: A cost-plus-profit sale contract where the bank buys the property and resells it to the customer at an agreed markup.

- Tawarruq: A more complex process involving the purchase and resale of commodities to generate liquidity in a Shariah-compliant manner.

These structures are crafted to avoid interest and instead rely on tangible asset transactions and transparent contractual obligations.

Example Products in the Market

Several Malaysian banks offer tailored Islamic financing products using these Shariah-compliant structures. Take, for instance, Maybank’s Commodity Murabahah Home Financing-i, where Maybank purchases commodities on behalf of the customer and sells them at an agreed profit rate3.

Similarly, Bank Muamalat’s Smart Mortgage Home delivers a flexible financing option embedded with profit-sharing features, full Islamic compliance, and integrated takaful protection4.

Key Differences Between Islamic and Conventional Housing Loans

Understanding what separates Islamic financing from conventional loans is essential. In conventional loans, interest accrues on borrowed money. Islam forbids this, requiring lenders and buyers to engage in real asset trading instead5.

Shariah-compliant solutions shift financial risk equitably and avoid contracts with uncertainty (gharar), offering predictable outcomes for both banks and buyers.

Applied Islamic Finance Concepts: Beyond Theory

Islamic home financing isn’t a loose ethical code—it’s governed by well-defined jurisprudential and financial rules. Core values include contract clarity and accountability. Risk and reward are shared and must be asset-linked6.

Several contract models ensure Shariah integrity, including BBA, Ijarah Muntahiyah Bi Tamlik, and Musharakah Mutanaqisah—each selected based on the region and consumer profile.

The Reform Imperative: Is Today’s Islamic Home Financing Truly Shariah-Compliant?

Although many products meet technical compliance standards, critiques persist that actual implementation often mirrors conventional debt structures—undermining Islamic economic justice7.

Scholars call for deeper integration of values and greater transparency. Key reforms include more visible scholar involvement and better consumer education8.

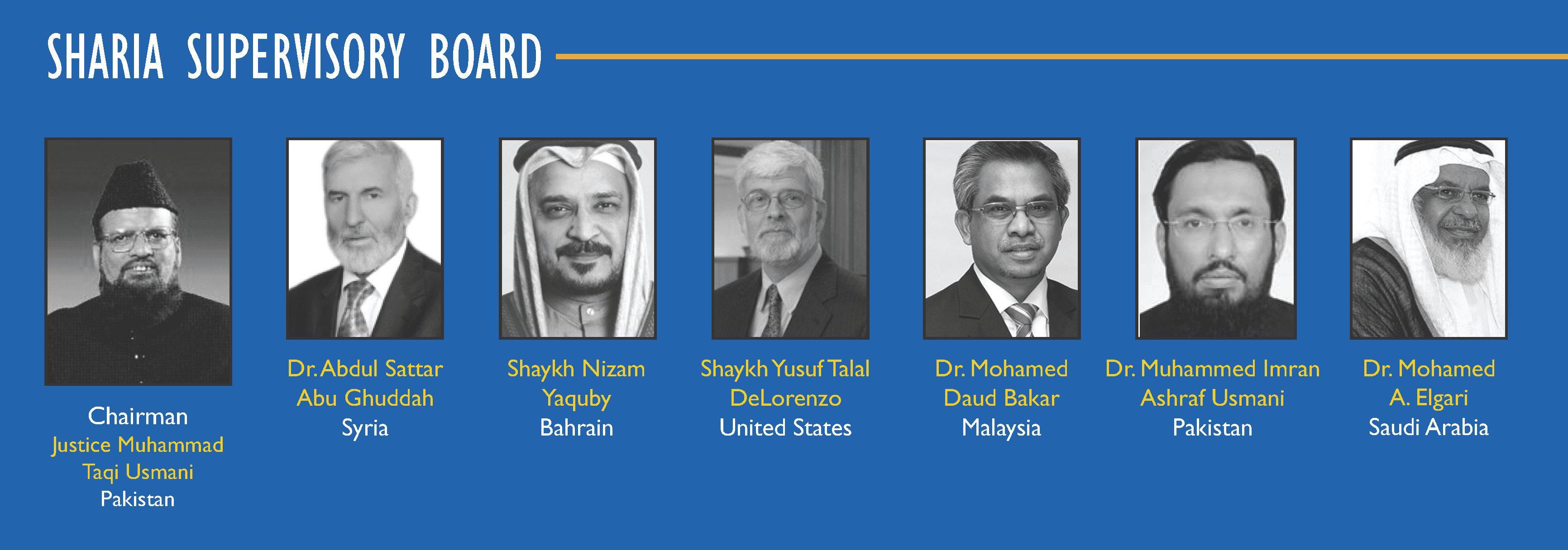

The Role of Shariah Supervisory Boards

Shariah Supervisory Boards (SSBs) work as regulatory guardians, ensuring Islamic financial product offerings maintain ethical authenticity. Their review helps maintain market confidence9.

{kind=link}

Without qualified and active boards, products risk being reduced to symbolic gestures disconnected from Shariah intent.

Consumer Behavior and Perceptions

Studies indicate Muslim consumers choose Islamic mortgages out of religious duty, but economic appeal like transparency, competitive pricing, and flexibility also play a vital role10.

However, skepticism arises when Islamic products feel rebranded from conventional formats, which underscores the importance of real structural differences.

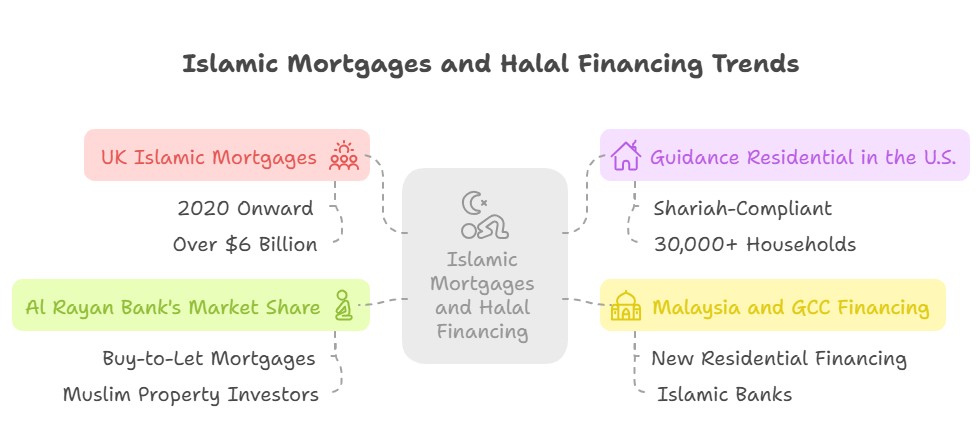

Singapore’s Islamic Mortgage Milestone

Singapore’s introduction of Shariah-compliant home financing shows that Islamic financial models are adaptable in secular and urban financial hubs. This signals wider industry receptiveness11.

As Muslim populations increase globally, Western markets may follow the same path toward inclusive home financing offerings.

Debunking Misconceptions: Is Real Estate Halal?

Real estate investment is halal if pursued under principles avoiding interest and uncertainty. Islamic mortgage models rely on trade, not debt mechanisms12.

Visual resources and community threads affirm that Islamic finance, when structured correctly, supports faith-compliant wealth-building13.

{kind=link}

Where Can You Explore Shariah-Compliant Properties?

Platforms like PropertyGuru help connect home seekers with Shariah-compliant listings, financing calculators, and property valuations. Their tools clarify the financial process while honouring Islamic principles14.

Muslim buyers are best served by using dedicated resources that accommodate Islamic financing options alongside conventional ones.

Frequently Asked Questions

Question: What makes an Islamic housing loan different from a conventional one?

Answer: Islamic housing loans avoid interest and instead engage in real trade transactions or profit-sharing models to achieve compliance with Shariah.

Question: Can non-Muslims apply for Shariah-compliant home financing?

Answer: Yes, non-Muslims can apply and benefit from these ethical, interest-free financial structures offered by Islamic banks.

Question: Are Islamic mortgage rates fixed or floating?

Answer: It depends on the contract. Certain models, like Murabahah, offer fixed profit rates, while others may adjust based on benchmark rates within Shariah boundaries.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.