.webp)

.webp)

Shariah-Compliant Home Financing: Building Trust and Ownership the Ethical Way

Key Takeaways

- Faith-Based Financing: Shariah-compliant home financing avoids interest and prioritizes ethical financial models under Islamic law.

- Growing Market: Islamic home financing is becoming more widely available across Malaysia and Singapore.

- Challenges & Calls for Reform: Concerns remain over authenticity, contract clarity, and Shariah compliance in current offerings.

Faith Meets Finance: The Rise of Shariah-Compliant Home Loans

As homeownership remains one of the most important steps in financial security and personal growth, Muslim buyers increasingly seek options that align with their ethical and spiritual commitments. Shariah-compliant home financing eliminates interest (riba), instead using sales-based or lease-based structures that comply with Islamic principles1.

Understanding the Structures That Make It Halal

Rather than a simple lender-borrower dynamic, Islamic home financing uses alternative modes like Murabahah, Ijarah, or Tawarruq where the bank either leases the property to the buyer or sells at a disclosed markup. These contracts remove the element of unjust enrichment linked with interest-based loans2.

Malaysia’s Institutional Commitment to Islamic Financial Ethics

Major banks like Maybank Islamic and Bank Muamalat lead the way in developing sophisticated Shariah-compliant home financing products. Through structured trading of commodities and transparent contracts, these financial institutions are actively integrating faith-based systems into mainstream banking3.

Smart Mortgage and Flexible Repayments

Borrowers in Malaysia can also benefit from innovative options like Muamalat’s Smart Mortgage Home, which allows early settlement without penalty, increasing accessibility while staying within the limits of Islamic jurisprudence4.

Going Beyond Borders: Singapore's First Islamic Mortgage

Singapore has become Southeast Asia’s next Islamic financing hotspot with the inauguration of its first fully Shariah-compliant property financing tool, designed to serve its Muslim population ethically and transparently5.

.webp)

Justice and trust are key pillars in Islamic home financing, driving the call for reform in Malaysia to ensure stronger compliance with Shariah principles and greater consumer protection. Ethical financial systems rooted in religious frameworks emphasize transparency, fairness, and accessibility in property ownership.

When Labels Don’t Match Practice: The Trust Issue

Despite the rise in popularity, critics argue that many so-called Islamic home financing schemes deviate from the foundational Shariah principles, often emulating conventional interest-based models with minor tweaks to terminology6.

Are We There Yet? The Call for Improvement

Academics and financial industry professionals advocate for deeper reforms and better training for Shariah boards to ensure full compliance, transparency, and consumer protection from misleading products7.

Solutions in Motion: Innovations in Contract Design

New and improved structures are being proposed to align even closer with Islamic financial ethics, including simplified Tawarruq mechanisms and rental restructuring strategies in Ijarah-based offerings8.

{kind=link}

Mitigating Risks: Avoiding Shariah Breaches

Financial experts warn against any income derived from contracts that fail to satisfy Shariah requirements, urging strict controls and compliance audits throughout the product lifecycle9.

The Guardians of Compliance: Role of Shariah Boards

Certified Shariah boards are responsible for validating the religious fidelity of each product and ensuring the integrity of the financial models offered to the public10.

Learning Curve: Educating the Buyers and Bankers

Financial education initiatives are essential to bridge information gaps, addressing buyers’ uncertainty and encouraging confident participation in Islamic home financing11.

Greener and Halal: The New Standard in Ethical Living

Eco-conscious platforms like Property Guru now offer green-certified and Shariah-compliant financing side-by-side, helping users make value-driven housing decisions without compromising on beliefs12.

Voices from the Ground: What People Think

Online communities reflect real-world concerns and compliments—people appreciate the ethics of Islamic loans but consistently ask for more clarity, fair pricing, and user-friendly contracts13.

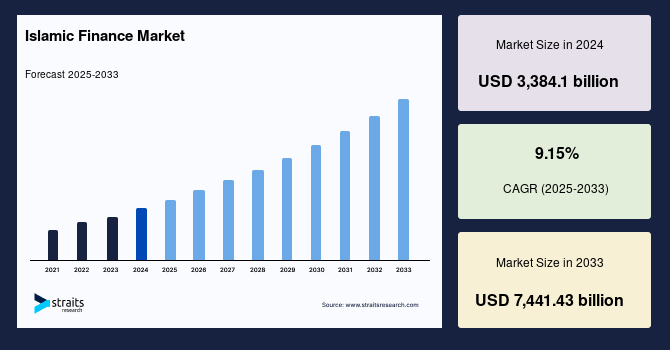

Market Momentum: Global Growth for Islamic Finance

The Islamic finance market is projected to reach new heights by 2033, with billions in assets under management and growing demand from ethically minded consumers around the world14.

{kind=link}

Frequently Asked Questions

Question: What makes a home loan Shariah-compliant?

Answer: A Shariah-compliant loan avoids interest payments and structures profit through sales or leasing contracts under Islamic rules.

Question: Are Islamic home financing options more expensive?

Answer: They may appear costlier upfront but include ethical features like risk sharing, transparency, and no penalties on early settlement.

Question: Can non-Muslims apply for Shariah-compliant housing loans?

Answer: Yes, Shariah-compliant products are available to all customers who prefer ethical and interest-free contracts.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.