)

.webp)

Shariah-Compliant Home Financing: A Rising Trend Reshaping Modern Property Ownership

Key Takeaways

- Ethical Financing Model: Shariah-compliant home financing avoids interest and focuses on fairness and shared risk.

- Different Structure: Islamic financing is asset-based rather than debt-based, involving real ownership or trade contracts.

- Growing Popularity: Increasing demand in regions like Southeast Asia reflects a shift toward ethical financial solutions.

- Governance Matters: Shariah boards ensure compliance and maintain trust in Islamic financial products.

- Future Potential: The sector is expected to grow with innovation, regulation, and broader adoption.

Introduction to Shariah-Compliant Home Financing

)

Modern residential developments reflecting ethical and value-driven property ownership concepts

In recent years, Shariah-compliant home financing has moved from a niche financial option to a fast-growing global trend. As more people look for ethical and interest-free ways to buy homes, Islamic finance is stepping into the spotlight—especially in regions like Malaysia and Southeast Asia.

This approach to financing is built on Islamic principles that prohibit interest and instead promote transparency, shared responsibility, and asset-backed transactions. It represents a broader shift toward values-driven finance, where buyers are not just concerned with affordability, but also with how their financial decisions align with ethical beliefs.

What Is Shariah-Compliant Home Financing?

At its core, Shariah-compliant home financing follows Islamic law, which prohibits interest (riba) and emphasizes fairness and shared risk between all parties involved. Instead of lending money with interest, financial institutions structure transactions around tangible assets1.

These financing models rely on contracts such as Murabahah, Musharakah, and Ijarah, allowing buyers and banks to engage in partnerships, leasing, or cost-plus sales. This ensures that the transaction remains tied to a real asset rather than speculative financial gain.

In simple terms, conventional loans involve borrowing money with interest, while Islamic financing focuses on buying, selling, or co-owning property under mutually agreed terms.

Islamic vs Conventional Home Loans: What’s the Real Difference?

The difference between Islamic and conventional home loans may appear subtle on the surface, but it is fundamentally structural. Islamic financing is trade-based, where profit is agreed upon upfront instead of fluctuating with interest rates2.

Additionally, discussions within Malaysia highlight that even if monthly payments look similar, the underlying mechanism is different, focusing on asset ownership rather than debt obligations3.

- No interest (riba)

- Shared risk between bank and buyer

- Asset-backed transactions

- Ethical investment approach

This distinction is a major reason why such financing models are gaining traction beyond religious communities.

Real-World Products: How Islamic Home Financing Works Today

Shariah-compliant financing is already widely implemented by financial institutions. For example, some banks use commodity-based structures where assets are bought and resold to customers at a predetermined profit margin4.

Other institutions offer flexible mortgage products that remain compliant while providing modern features such as payment flexibility and customization5.

These examples demonstrate how Islamic finance is evolving to meet contemporary housing demands without compromising its foundational principles.

A Growing Regional Movement

The growth of Shariah-compliant home financing is not confined to one country. While Malaysia has long been a leader in this space, other regions are beginning to adopt similar frameworks, including new initiatives emerging in Singapore6.

This expansion reflects a broader demand for ethical financial systems and inclusive banking solutions that cater to diverse populations.

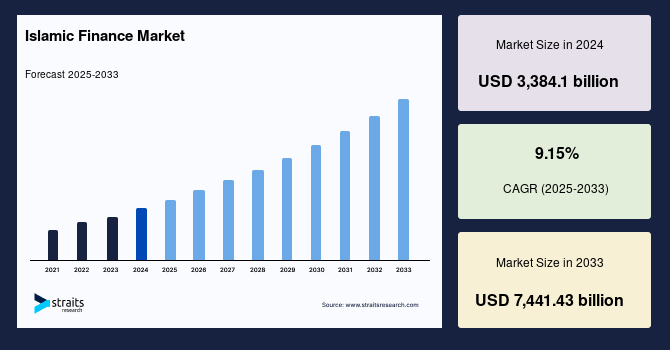

Globally, the Islamic finance market continues to show strong growth potential, supported by increasing awareness and demand for alternative financing models7.

{kind=link}

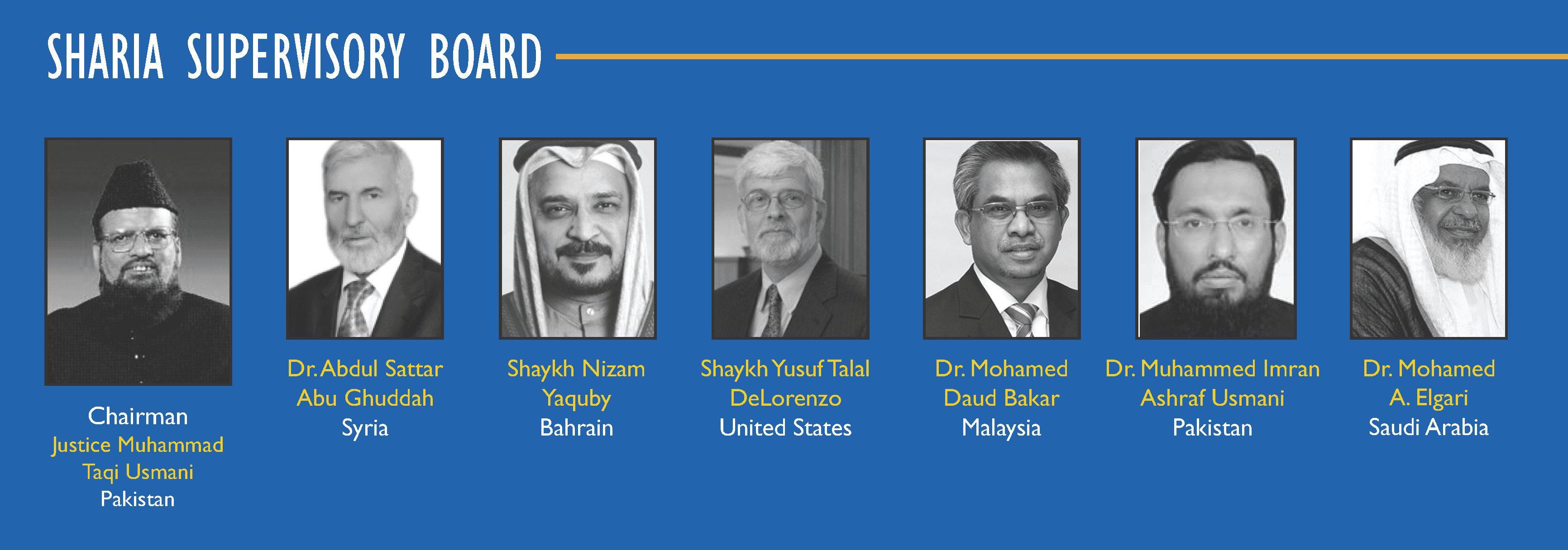

The Role of Shariah Boards: Who Ensures Compliance?

A critical component of Islamic finance is governance through Shariah boards. These boards consist of scholars who evaluate and certify financial products to ensure they comply with Islamic principles8.

{kind=link}

Their responsibilities include reviewing contracts, auditing transactions, and ensuring that institutions adhere strictly to Shariah guidelines. This oversight is essential in maintaining trust and credibility within the industry.

Challenges: Is Islamic Home Financing Always Truly “Islamic”?

Despite its growth, the industry faces challenges related to authenticity. One concern is the presence of Shariah Non-Compliance Income (SNCI), which can arise in certain complex financing structures9.

Researchers continue to explore ways to strengthen compliance, focusing on improving governance frameworks, refining product structures, and increasing transparency10.

Ongoing academic work also highlights the importance of ensuring that products do not merely replicate conventional loans under different names11.

Justice, Trust, and the Call for Reform

The discussion around Shariah-compliant financing extends beyond technical structures into ethical considerations. Experts emphasize the need for justice, fairness, and genuine adherence to Islamic values in financial practices12.

This includes avoiding structures that mimic interest-based systems, ensuring fair pricing, and prioritizing consumer protection. The focus is shifting toward authenticity rather than mere compliance.

Why More Homebuyers Are Paying Attention

The increasing interest in Shariah-compliant home financing is driven by a combination of ethical awareness, financial transparency, and inclusivity. In 2026, more buyers are actively seeking financial solutions that align with their personal values while offering stability and predictability.

- Ethical finance aligned with personal beliefs

- Transparent profit structures

- Increased accessibility for underserved groups

What This Means for the Future of Property Buying

The continued rise of Shariah-compliant financing is likely to reshape the property market. As demand increases, financial institutions are expected to introduce more innovative products while regulators enhance oversight.

- Expansion of Islamic financial products

- Greater competition with conventional loans

- Stronger regulatory frameworks

For homebuyers, this means more diverse options that align with both financial goals and ethical considerations.

Final Thoughts: A Financial System in Transition

Shariah-compliant home financing is no longer just an alternative—it is becoming a significant force in the global financial system. Its emphasis on fairness, transparency, and shared responsibility resonates with a growing number of buyers.

As the industry evolves, maintaining authenticity and trust will be essential. When implemented effectively, this model offers more than just a financing option—it provides a framework for ethical and sustainable property ownership.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional loans?

Answer: It avoids interest and instead uses asset-based contracts where the bank and buyer share ownership or engage in trade-based agreements.

Question: Is Shariah-compliant financing only for Muslims?

Answer: No, it is open to anyone interested in ethical and transparent financial solutions, regardless of religious background.

Question: Are Islamic home financing payments cheaper than conventional loans?

Answer: Not necessarily; payments can be similar, but the key difference lies in the structure and ethical foundation of the financing.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.