)

.webp)

Shariah-Compliant Home Financing: The Future of Ethical Homeownership in 2026

Key Takeaways

- Interest-Free Structure: Shariah-compliant financing avoids riba by using asset-based transactions instead of loans.

- Multiple Financing Models: Common structures include Murabahah, Ijarah, and Tawarruq, each offering different ownership paths.

- Growing Global Demand: Ethical finance trends and rising housing costs are driving increased adoption worldwide.

- Governance Matters: Shariah Boards play a crucial role in ensuring compliance, transparency, and trust.

- Challenges Remain: Issues like transparency, consumer understanding, and standardization still need improvement.

What Is Shariah-Compliant Home Financing?

In 2026, Shariah-compliant home financing is no longer a niche topic—it is one of the fastest-growing conversations in global finance. As housing costs rise and ethical investing gains attention, more people are exploring alternatives to conventional mortgages that avoid interest-based debt structures.

At its core, this model is built on the principle of no riba (interest). Instead of lending money, financial institutions engage in trade-based or lease-based agreements where assets are central to the transaction1.

The most common structures include Murabahah, where a bank sells a property at a markup, Ijarah, which operates like leasing with eventual ownership, and Tawarruq, a more complex commodity-based structure. Each approach emphasizes fairness, transparency, and shared responsibility.

There is also growing overlap with sustainable housing trends, where ethical finance meets environmentally conscious property development2.

Real-World Examples of Islamic Home Financing

Major banks have already integrated Shariah-compliant products into their offerings, showing how these models work in practice. These products replace traditional interest with clearly defined profit margins tied to real assets.

Some institutions structure financing through commodity-based transactions to ensure compliance while maintaining competitive pricing and accessibility3.

Others design home financing solutions specifically tailored for ethical homeownership, demonstrating how Islamic finance adapts to modern housing needs without compromising principles4.

Why Shariah Compliance Matters More in 2026

The rise of Shariah-compliant financing is closely tied to global demand for ethical financial systems. Increasing awareness around fairness, combined with rising property prices, has pushed buyers to consider alternatives beyond conventional loans.

Research shows that Islamic finance aims to balance economic growth with moral values, making it appealing not just to Muslims but to a broader audience seeking transparency and accountability5.

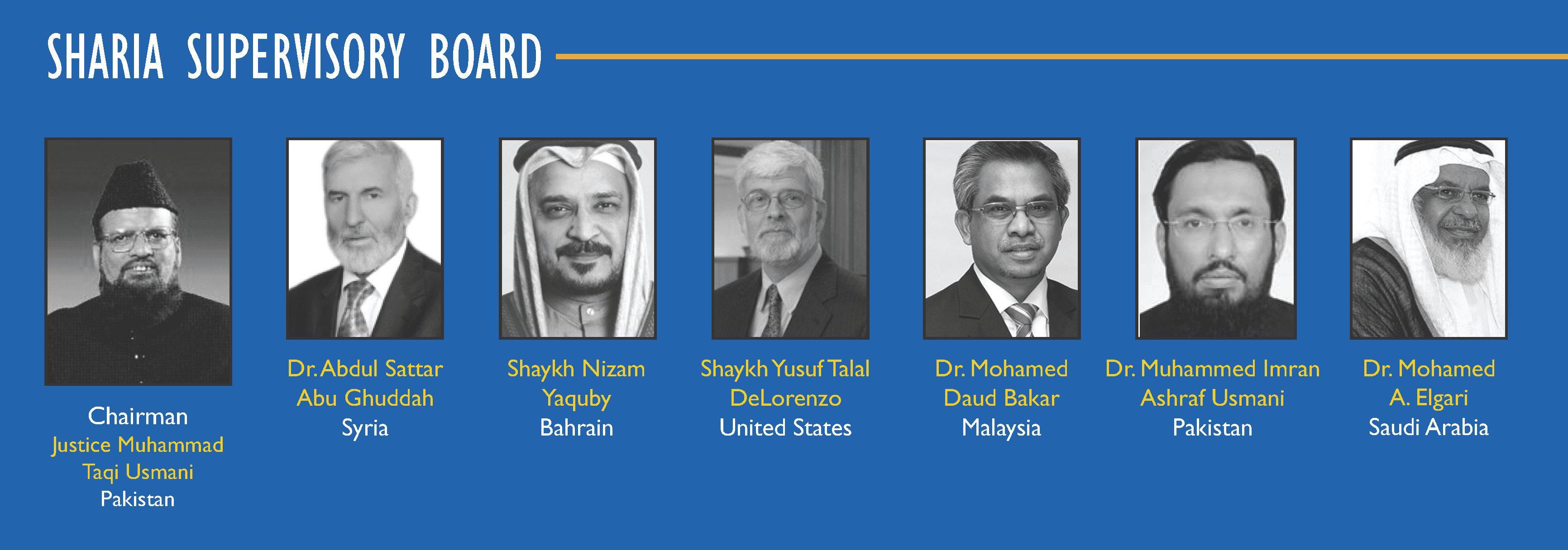

The Role of Shariah Boards: Guardians of Trust

)

Scholarly governance structure overseeing ethical compliance in Islamic financial systems

Shariah Boards are central to ensuring that financial products comply with Islamic principles. These groups of scholars review, audit, and approve structures to ensure ethical integrity and transparency across transactions6.

{kind=link}

However, ongoing discussions highlight the need for stronger governance and improved transparency to maintain long-term trust in the system7.

The Transparency Challenge: Is Everything Truly Halal?

Despite its growth, not all Islamic financing models are universally accepted. Structures like Tawarruq have sparked debate among scholars regarding their compliance and ethical validity.

Some studies suggest that certain transactions may unintentionally generate non-compliant income, raising concerns about whether all products fully meet Shariah standards8.

The Knowledge Gap: Why Many Buyers Still Feel Confused

Consumer understanding remains a major challenge. Many buyers find it difficult to grasp how Islamic home financing works compared to conventional mortgages.

Research indicates that confusion around product structures and lack of clarity in contracts can lead to mistrust and hesitation among potential buyers9.

Legal awareness also plays a role, as insufficient understanding of rights and obligations can further complicate decision-making10.

How Payment Structures Differ from Conventional Mortgages

One of the key differences lies in payment structures. Instead of paying interest, buyers agree to a profit margin or rental-based payment tied to the asset itself.

This structure provides predictability and avoids compounding interest, although some critics argue that total costs may still resemble traditional loans in practice11.

{kind=link}

Innovation Is Driving the Next Wave

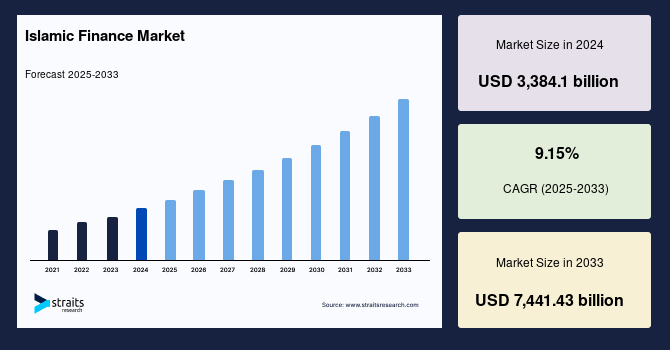

Technology is rapidly transforming the Islamic finance landscape. Digital platforms now allow users to compare options, automate compliance checks, and access transparent financing solutions.

At the same time, global market data shows strong growth, driven by demographic trends and increasing demand for ethical finance solutions12.

{kind=link}

The Push for Better Shariah Compliance

Researchers and regulators are working to improve the structure and governance of Islamic home financing. The goal is to reduce ambiguity and enhance trust through clearer standards and consistent frameworks.

Improved methodologies and continuous scholarly oversight are seen as essential steps toward strengthening the system13.

Why This Trend Matters Beyond Religion

Even beyond religious considerations, Shariah-compliant financing introduces ideas that challenge traditional lending systems. Its focus on fairness, shared risk, and transparency resonates with a wider audience seeking alternatives to debt-heavy models.

This aligns closely with broader movements toward ethical and sustainable financing in the housing sector14.

The Road Ahead: What to Expect Next

Looking ahead, Shariah-compliant home financing is expected to expand globally, supported by fintech innovation, improved regulation, and greater consumer awareness.

While challenges such as transparency and education remain, ongoing developments suggest a more refined and accessible system in the years to come.

Final Thoughts

Shariah-Compliant Home Financing represents a shift toward ethical, transparent, and accountable financial systems. It offers an alternative path to homeownership that challenges conventional assumptions about lending.

As the industry evolves, its true impact will depend on how well it balances growth with integrity, ensuring that its principles are not only preserved but strengthened over time.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional mortgages?

Answer: It avoids interest and instead uses asset-based structures like buying, leasing, or profit-sharing agreements to finance property.

Question: Is Shariah-compliant financing only for Muslims?

Answer: No, it is open to anyone interested in ethical, transparent financial solutions regardless of religion.

Question: Are Islamic home financing options more expensive?

Answer: Not necessarily, although total costs can sometimes be similar to conventional loans depending on the structure and market conditions.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.