)

.webp)

Shariah-Compliant Home Financing: The Rising Global Shift in Ethical Property Ownership

Key Takeaways

- Ethical Financing Growth: Shariah-compliant home financing is rapidly expanding as demand for transparent and interest-free solutions increases.

- Different Structure: Islamic financing replaces interest-based loans with trade or partnership models.

- Malaysia’s Leadership: Malaysia is a global hub driving innovation in Islamic home financing products.

- Trust Challenges: Questions around authenticity and compliance remain a key concern for consumers.

- Future Outlook: The sector is evolving toward greater transparency, regulation, and global adoption.

What Is Shariah-Compliant Home Financing?

Shariah-compliant home financing follows Islamic finance principles that prohibit interest (riba), promote shared risk, and require transactions to be backed by real assets. Instead of lending money with interest, financial institutions use structures such as partnerships or cost-plus sales to facilitate home ownership1.

This approach fundamentally changes how buyers interact with financing. Rather than simply repaying a loan, buyers participate in structured agreements where ownership is gradually transferred or assets are traded transparently, creating a more ethical and asset-driven system2.

Why Is It Trending Now?

The rise of Shariah-compliant home financing in 2026 is driven by both religious and ethical considerations. While Muslim buyers seek alignment with their beliefs, non-Muslims are increasingly drawn to its transparency and fairness.

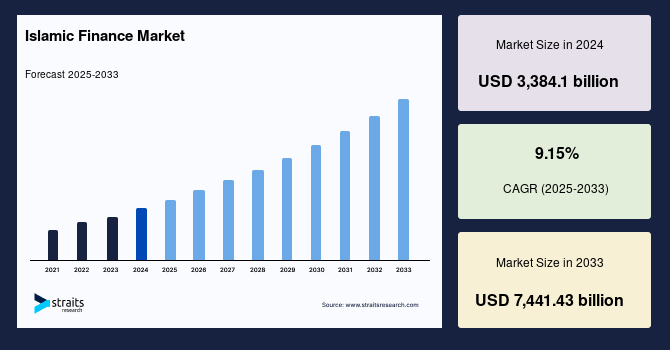

At the same time, the global Islamic finance market is expanding rapidly, signaling a broader shift toward ethical financial systems that prioritize accountability and real economic activity3.

{kind=link}

Malaysia: A Leader in Islamic Home Financing Innovation

Malaysia has positioned itself as a global leader in Islamic finance, offering a wide range of Shariah-compliant home financing products tailored to modern buyers. Financial institutions have introduced specialized offerings designed specifically for halal property ownership4.

These products are built using concepts like Murabahah, Musharakah, and Ijarah, which redefine ownership, payment structures, and risk-sharing. Despite this innovation, maintaining strict adherence to Shariah principles remains an ongoing challenge in the industry.

The Big Question: Are All Islamic Mortgages Truly Shariah-Compliant?

Not all products labeled as Islamic fully meet Shariah standards in practice, raising concerns about authenticity and transparency within the industry5.

Scholars and researchers emphasize the need for stronger governance frameworks to ensure these products genuinely follow Islamic principles rather than merely replicating conventional loan structures6.

)

Framework illustrating governance, compliance layers, and ethical oversight in Islamic home financing systems

Experts also highlight the importance of reforming industry practices to rebuild trust and ensure fairness in how these financial products are structured and delivered7.

Consumer Trust: The Hidden Challenge

Despite strong growth, many consumers remain uncertain about how Islamic home financing differs from conventional loans. Online discussions reveal confusion about whether these products truly offer better value or simply mirror traditional systems8.

Research shows that trust increases significantly when financing options are transparent, clearly structured, and genuinely compliant with Shariah principles, highlighting the importance of clarity in driving adoption9.

Inside the Most Common Islamic Financing Models

Islamic home financing relies on several core models that replace traditional interest-based lending with ethical alternatives.

Murabahah involves the bank purchasing a property and selling it to the buyer at a profit margin, with payments made over time. This structure is widely used in modern Islamic banking systems10.

Musharakah operates as a partnership where both the buyer and the bank co-own the property, and ownership gradually shifts to the buyer over time.

Tawarruq, a more complex structure, involves commodity transactions to create liquidity, but it has sparked debate due to potential compliance risks and concerns around non-compliant income11.

Beyond Malaysia: A Regional Movement

The adoption of Shariah-compliant home financing is spreading across Southeast Asia, with countries like Singapore introducing new offerings that reflect growing regional demand12.

This expansion signals a broader shift toward ethical financing ecosystems, where competition is expected to improve product quality, compliance, and accessibility.

Comparing Islamic vs Conventional Home Loans

Conventional home loans are built on interest-based lending, where borrowers repay the principal along with interest, and most of the financial risk is carried by the borrower.

In contrast, Shariah-compliant financing avoids interest, emphasizes shared risk, and ensures that transactions are tied to real assets. However, the overall cost may sometimes appear similar, which can lead to confusion among buyers.

The Role of Technology in Islamic Finance

Technology is increasingly shaping the future of Islamic finance by making complex structures easier to understand and more accessible to consumers.

Digital platforms are helping simplify processes, improve transparency, and provide better educational tools, allowing buyers to make more informed decisions about their financing options.

What This Means for Home Buyers

Shariah-compliant home financing presents a viable alternative for buyers seeking ethical and transparent solutions, but it requires careful evaluation.

Understanding the structure, profit calculation, ownership transfer process, and certification of each product is essential to making the right decision.

The Future of Ethical Home Financing

The future of Shariah-compliant home financing points toward greater standardization, stronger regulatory frameworks, improved consumer awareness, and wider global adoption.

As the industry evolves, maintaining authenticity and building trust will be critical to sustaining long-term growth.

Final Thoughts

Shariah-compliant home financing is no longer a niche concept. It represents a meaningful shift toward ethical, transparent, and values-driven financial systems.

As adoption grows across regions, the focus must remain on ensuring that every product genuinely reflects the principles it claims to uphold.

Ultimately, the success of this movement will depend on trust, accountability, and the ability to deliver truly ethical home ownership solutions.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional loans?

Answer: Shariah-compliant financing avoids interest and instead uses trade or partnership-based structures that involve shared risk and real asset transactions.

Question: Is Shariah-compliant home financing only for Muslims?

Answer: No, it is open to anyone. Many non-Muslims choose it for its ethical principles, transparency, and structured approach to financing.

Question: Are Islamic home financing products always cheaper than conventional loans?

Answer: Not necessarily. While the structure is different, the overall cost can sometimes be similar, depending on the product and market conditions.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.