)

.webp)

Shariah-Compliant Home Financing: How Malaysia Is Reshaping Ethical Homeownership in 2026

Key Takeaways

- Ethical Financing Model: Shariah-compliant home financing avoids interest and promotes fairness through asset-based transactions.

- Malaysia’s Leadership: The country continues to lead global Islamic finance innovation with reforms focused on transparency and trust.

- Diverse Financing Structures: Models like Murabahah and Tawarruq offer flexible alternatives to conventional mortgages.

- Growing Demand: Rising awareness and ethical preferences are driving increased adoption among modern homebuyers.

- Future-Focused Reforms: Regulatory improvements and digital transformation are shaping the next phase of Islamic home financing.

Introduction to Shariah-Compliant Home Financing

)

Modern residential developments reflecting ethical property ownership and financial inclusivity in Malaysia

Shariah-compliant home financing in Malaysia is evolving as a key model for ethical homeownership, emphasizing risk-sharing, asset-backed transactions, and the avoidance of interest. The system reflects a broader movement toward transparency, fairness, and financial practices aligned with Islamic principles while adapting to modern economic demands1.

This shift is gaining momentum in 2026, with Malaysia positioned at the forefront of innovation in Islamic finance, offering a system that blends faith-based values with practical solutions for today’s property market.

What Is Shariah-Compliant Home Financing?

At its core, Shariah-compliant home financing avoids interest (riba) and instead relies on structured transactions tied to real assets. Rather than lending money, financial institutions engage in trade-based or partnership-based agreements that ensure fairness and shared responsibility2.

This approach creates a more transparent system where both the bank and the buyer participate in the transaction, aligning financial outcomes with ethical considerations.

Why Shariah-Compliant Home Financing Is Trending in 2026

Malaysia’s Islamic finance sector is entering a new phase where reform is becoming just as important as growth. Industry discussions increasingly focus on improving transparency, fairness, and consumer trust to better reflect core principles of justice and accountability3.

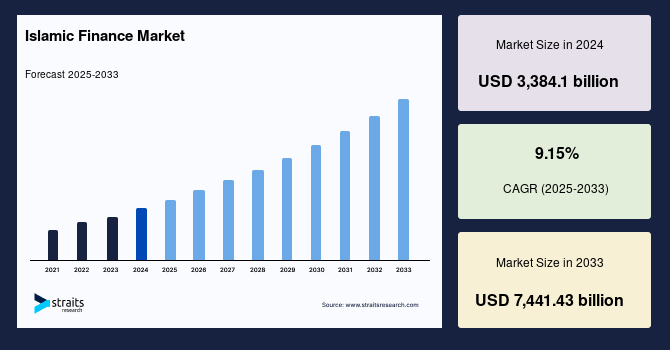

At the same time, global demand for ethical financial systems continues to rise, with Islamic finance expected to expand significantly in the coming years, strengthening the relevance of Shariah-compliant home financing4.

{kind=link}

The Core Structures Behind Islamic Home Financing

Commodity Murabahah

This widely used structure involves the bank purchasing a commodity and selling it to the customer at a profit margin, with payments made over time. It enables homeownership without relying on interest-based lending5.

Tawarruq-Based Financing

Tawarruq structures provide liquidity through a series of transactions, but they require careful monitoring to avoid Shariah non-compliance issues such as unintended income elements that do not meet ethical standards6.

Custom Financing Solutions

Banks are increasingly offering tailored Islamic financing options designed to meet diverse customer needs while maintaining strict adherence to ethical guidelines7.

The Role of Major Banks in Malaysia

Leading financial institutions play a central role in advancing Islamic home financing by offering competitive and compliant property financing solutions that cater to both residential and commercial buyers8.

These institutions are helping bring Islamic finance into the mainstream by improving accessibility and offering flexible solutions for a wide range of customers9.

Challenges Facing Shariah-Compliant Home Financing

Despite its benefits, Islamic home financing still faces challenges related to consumer understanding and transparency. Many buyers find the structures complex, which can affect trust and adoption rates10.

There are also ongoing debates about whether certain financing models closely resemble conventional loans, highlighting the need for continuous improvement and stricter adherence to core principles11.

Why Reform Is Critical Right Now

Reform efforts are focused on strengthening the integrity of Islamic finance by aligning practices more closely with foundational values such as fairness, trust, and accountability, ensuring long-term sustainability and global competitiveness.

How This Affects Homebuyers

- Ethical Financing: Buyers can access interest-free structures aligned with religious values.

- Transparent Agreements: Clearly defined profit margins improve financial clarity.

- More Choices: Increasing product diversity allows better customization.

- Complex Structures: Understanding different models may require additional research.

The Bigger Picture: Global Islamic Finance Growth

The expansion of Islamic finance globally highlights the growing demand for ethical financial systems, with Malaysia serving as a benchmark for innovation and implementation in this space.

What the Future Looks Like

- Greater Transparency: Simplified structures and clearer communication for consumers.

- Stronger Compliance: Enhanced monitoring systems to ensure ethical integrity.

- Digital Innovation: Technology-driven processes improving accessibility and efficiency.

- Personalized Solutions: More tailored financing products for diverse buyer needs.

Final Thoughts

Shariah-compliant home financing is more than a financial alternative—it represents a shift toward ethical, transparent, and inclusive homeownership. Malaysia’s continued leadership in this space reflects its commitment to innovation while staying true to foundational values.

As the system evolves, it offers both opportunities and responsibilities for homebuyers, financial institutions, and regulators alike, shaping the future of property ownership on a global scale.

Frequently Asked Questions

Question: What makes Shariah-compliant home financing different from conventional loans?

Answer: It avoids interest and instead uses asset-based or trade-based contracts, ensuring ethical and transparent financial transactions.

Question: Is Shariah-compliant home financing only for Muslims?

Answer: No, it is open to anyone interested in ethical financing options that emphasize fairness and transparency.

Question: Are Islamic home financing products more complicated?

Answer: They can be more complex due to different contract structures, but increased transparency efforts are making them easier to understand.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.