)

.webp)

Shariah-compliant home financing: A closer look at ethical homeownership in 2026

Key Takeaways

- Interest-Free Structure: Shariah-compliant financing avoids interest and uses asset-based transactions.

- Ethical Foundations: Built on fairness, transparency, and shared risk between bank and buyer.

- Malaysia Leads: The country remains a global hub for Islamic home financing innovation.

- Growing Demand: Rising awareness and ethical finance trends are driving adoption.

- Challenges Remain: Complexity, trust issues, and debates on authenticity continue to shape the industry.

Introduction to Shariah-compliant home financing

)

Modern residential developments reflecting ethical and structured approaches to homeownership financing

Shariah-compliant home financing is gaining serious attention in 2026 as more people rethink how money, fairness, and housing connect. What was once considered a niche offering is now steadily moving into the mainstream, especially in Malaysia.

At its core, this financing model focuses on purchasing a home without relying on interest, aligning financial transactions with Islamic principles. Instead of traditional lending, it introduces structured agreements rooted in shared responsibility, ethical practices, and asset-backed transactions.

What is Shariah-compliant home financing?

Shariah-compliant home financing is an alternative to conventional mortgages where interest is not charged. Instead, financing is structured through trade, leasing, or partnership models that link transactions directly to tangible assets.

A simple comparison explains the concept clearly: rather than borrowing money and paying interest, the buyer enters into an agreement where the bank participates in the property transaction and earns profit through predefined terms1.

This shift from money lending to asset-based dealings is what fundamentally differentiates Islamic home financing from conventional systems.

The key principles behind Islamic home financing

Islamic finance operates under Shariah law, which governs how financial products must be structured and executed. These principles ensure that every transaction is ethical, transparent, and tied to real economic activity.

The framework is reinforced through governance systems that monitor compliance and enforce accountability across financial institutions2.

- No interest (riba)

- Shared risk between parties

- Asset-backed transactions

- Clear and transparent agreements

Common structures used in Malaysia

Malaysia stands as a global leader in Islamic finance, offering a range of structured home financing solutions tailored to Shariah principles.

Commodity Murabahah (Tawarruq)

This widely used structure involves the bank purchasing a commodity and selling it to the customer at a marked-up price, which is then repaid in installments. The profit margin is agreed upfront, removing uncertainty associated with interest-based systems3.

Tawarruq-based financing

This structure enables liquidity while maintaining Shariah compliance, though it has sparked debate due to concerns around compliance risks such as unintended violations within transaction flows4.

Other bank offerings

Major banks in Malaysia continue to expand their Shariah-compliant product lines, offering diverse options with varying flexibility and pricing structures5.

Why demand is rising in 2026

The growth of Shariah-compliant home financing is driven by a broader shift toward ethical and transparent financial systems, appealing to both Muslim and non-Muslim consumers.

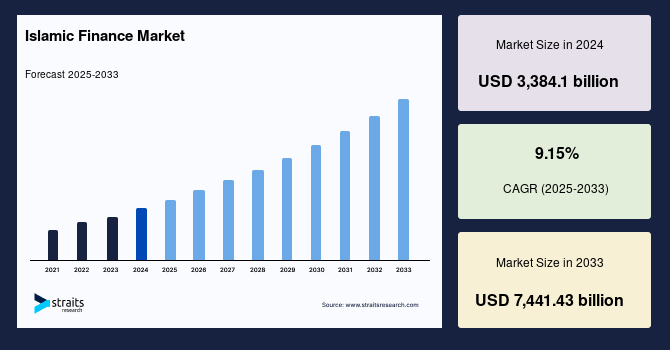

Global market expansion reflects increasing demand, with strong projections highlighting the continued rise of Islamic finance across multiple sectors6.

{kind=link}

In Malaysia, institutional support and policy frameworks further strengthen adoption, particularly in property financing solutions offered through Islamic banking platforms7.

The role of Shariah boards: Who ensures compliance?

Shariah boards play a critical role in overseeing Islamic financial products, ensuring that every structure adheres strictly to religious and ethical guidelines.

These boards review contracts, monitor operations, and safeguard consumer interests, forming the backbone of trust in Islamic finance systems8.

Consumer trust: A growing but fragile factor

While adoption is increasing, consumer trust remains a complex issue. Some buyers question whether certain products genuinely meet Shariah requirements or simply mirror conventional loans.

Research shows mixed perceptions, with concerns around transparency, pricing clarity, and contractual complexity continuing to influence decision-making9.

The reform debate: Justice, fairness, and transparency

Discussions in 2026 increasingly focus on reforming Islamic home financing to improve fairness and transparency within the system.

Key debates question whether pricing models are equitable and whether customers fully understand their agreements, highlighting the need for clearer structures and stronger governance10.

Comparing Islamic vs conventional mortgages

The distinction between Islamic and conventional mortgages lies in their underlying philosophy. Conventional systems rely on lending and interest, while Islamic financing is based on asset ownership and trade.

This fundamental difference reshapes how profit is generated and how risk is distributed between financial institutions and homebuyers.

Challenges in current models

Despite its benefits, Islamic home financing faces several challenges that impact adoption and perception.

Compliance risks remain a concern, particularly when transaction structures unintentionally deviate from Shariah requirements, raising questions about consistency and oversight11.

Innovation: What’s next for Shariah-compliant home financing?

Innovation is shaping the next phase of Islamic home financing, with a strong focus on authenticity and alignment with real economic activity.

New approaches are exploring improved rental structures that better reflect actual market conditions while reducing reliance on conventional financial benchmarks12.

{kind=link}

There is also a growing push toward enhancing authenticity, ensuring that products are not just technically compliant but genuinely aligned with Islamic financial principles13.

{kind=link}

What this means for homebuyers

For homebuyers in 2026, Shariah-compliant financing presents a viable and increasingly popular alternative to traditional mortgages.

- Understand the financing structure before committing

- Compare offerings across different banks

- Clarify profit rates and ownership terms

- Ensure alignment with personal financial values

The bigger picture: Finance, faith, and fairness

Shariah-compliant home financing goes beyond transactions. It reflects a broader vision of integrating faith, economics, and ethical responsibility into everyday financial decisions.

As Malaysia continues to lead in this space, the model serves as a real-world test of whether finance can balance profitability with fairness and accountability.

Final thoughts

Shariah-compliant home financing in 2026 is evolving rapidly, offering a strong alternative grounded in ethical and asset-based principles.

While growth and demand continue to rise, the industry must address ongoing concerns around transparency, trust, and true compliance.

The future lies in refining these systems to ensure they are not only compliant in structure but also genuinely fair, clear, and trustworthy in practice.

Frequently Asked Questions

Question: What makes Shariah-compliant financing different from conventional loans?

Answer: It avoids interest and instead uses asset-based agreements where profit is structured through trade, leasing, or partnership models.

Question: Is Shariah-compliant home financing only for Muslims?

Answer: No, it is open to anyone interested in ethical, transparent, and interest-free financing options.

Question: Are Islamic home financing products more expensive?

Answer: Costs vary depending on the structure and provider, but they are not necessarily more expensive and should be compared carefully with conventional options.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.