)

.webp)

Sharia-compliant Home Financing: A Simple Guide to Ethical Homeownership in 2026

Key Takeaways

- Interest-Free Financing: Sharia-compliant home financing avoids interest and focuses on ethical profit structures.

- Asset-Backed Transactions: Financing is based on real property ownership rather than lending money alone.

- Shared Risk Model: Banks and buyers share responsibility, creating a more balanced financial relationship.

- Ethical Framework: The system emphasizes fairness, transparency, and moral responsibility.

- Growing Global Demand: Increasing interest worldwide shows its appeal beyond religious boundaries.

Introduction to Sharia-compliant Home Financing

In 2026, Sharia-compliant home financing is no longer a niche topic but a rapidly growing global trend that is reshaping how people approach homeownership. Buyers today are not only concerned with owning property but also with ensuring that the process aligns with ethical and faith-based values rooted in fairness and responsibility1.

Across different regions, many individuals are exploring ways to own homes without engaging in interest-based transactions. This shift reflects a broader move toward financial systems that emphasize shared risk, transparency, and accountability rather than profit from lending alone.

What Is Sharia-compliant Home Financing?

Sharia-compliant home financing allows individuals to purchase property without using interest, which is prohibited in Islamic finance. Instead of traditional loans, banks use structured agreements based on trade and asset ownership, ensuring that profits are earned through legitimate economic activity2.

One common structure is the Murabahah model, where the bank purchases the property and sells it to the buyer at an agreed markup. Payments are made in fixed installments, creating clarity and eliminating uncertainty.

For those interested in combining ethical financing with sustainability, modern property solutions are also integrating environmentally conscious housing approaches into financing options3.

How Is It Different from a Conventional Mortgage?

Although both systems involve monthly payments and eventual ownership, the underlying structure differs significantly. Conventional mortgages are based on lending money with interest, while Sharia-compliant models are built on ownership, leasing, or partnership agreements4.

In Islamic financing, the bank either owns or co-owns the property, and the buyer pays rent or a profit margin instead of interest. Ownership is gradually transferred, ensuring that transactions are tied to real assets rather than purely financial instruments.

Visual comparisons of these systems further highlight the structural differences between conventional and Islamic mortgages5.

The Core Principles Behind Islamic Finance

Understanding Islamic finance requires familiarity with its core principles, which guide all financial transactions within the system. These include the prohibition of interest, avoidance of excessive uncertainty, and the requirement for ethical and asset-backed investments6.

- No interest (riba)

- No excessive uncertainty (gharar)

- No gambling or speculation

- Ethical and halal investments only

- Profit from real economic activity

- Shared risk between parties

Why Ethics Matter in Home Financing

Ethics play a central role in Sharia-compliant financing, focusing on justice, trust, and transparency in every transaction. These values are particularly important in property purchases, where long-term financial commitments are involved7.

In practice, this means clear agreements, fair pricing, and accountability for both parties. Buyers increasingly value these qualities, especially when making significant financial decisions such as purchasing a home.

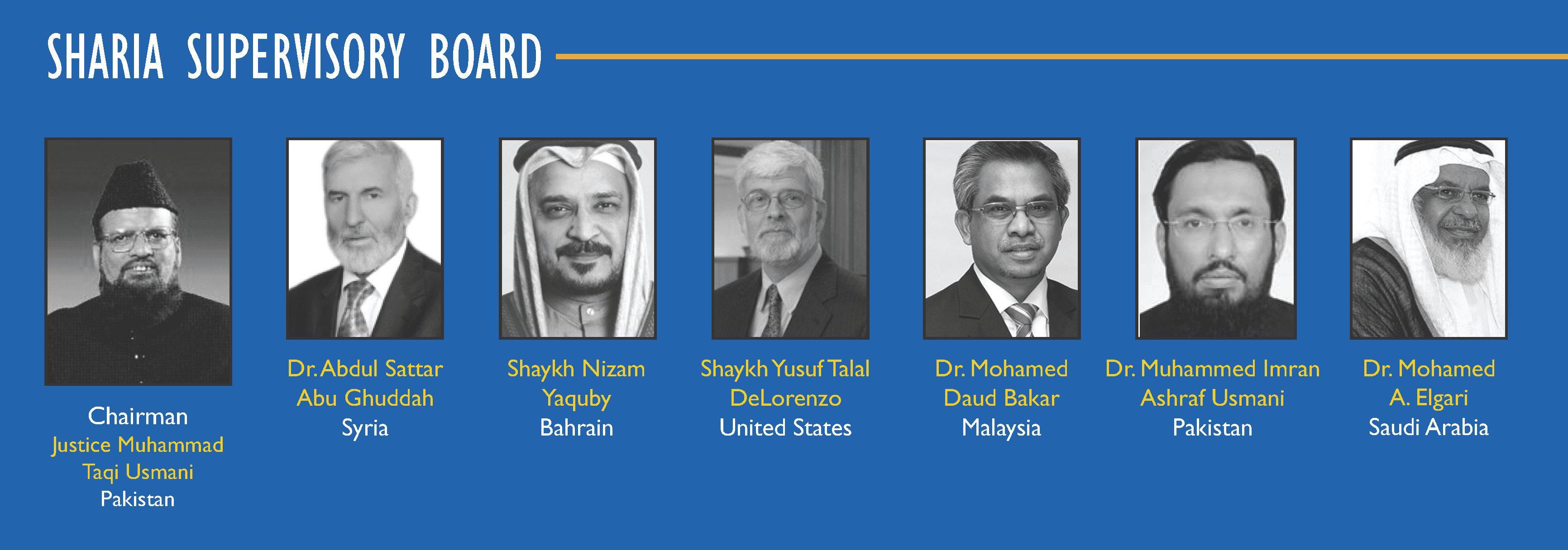

The Role of Shariah Boards

Shariah boards are essential to maintaining compliance within Islamic financial systems. These panels of scholars review contracts and financial products to ensure that they adhere strictly to Islamic principles8.

{kind=link}

By overseeing financial structures, they help prevent interest-based elements, reduce uncertainty, and maintain fairness across all agreements.

Types of Sharia-compliant Home Financing

There are several models used in Islamic home financing, each designed to align with Sharia principles while offering flexibility to buyers.

- Murabahah (Cost-Plus Financing)

- Ijarah (Lease-to-Own)

- Musharakah (Partnership)

Modern financial institutions continue to innovate within these frameworks, offering products that combine compliance with convenience9.

Is It Really Halal?

Sharia-compliant home financing is generally considered halal when structured correctly, meaning it avoids interest and ensures transparency and real asset involvement. However, discussions continue around certain products that closely resemble conventional loans10.

Educational resources and discussions also explore evolving perspectives on real estate and halal financing practices11.

{kind=link}

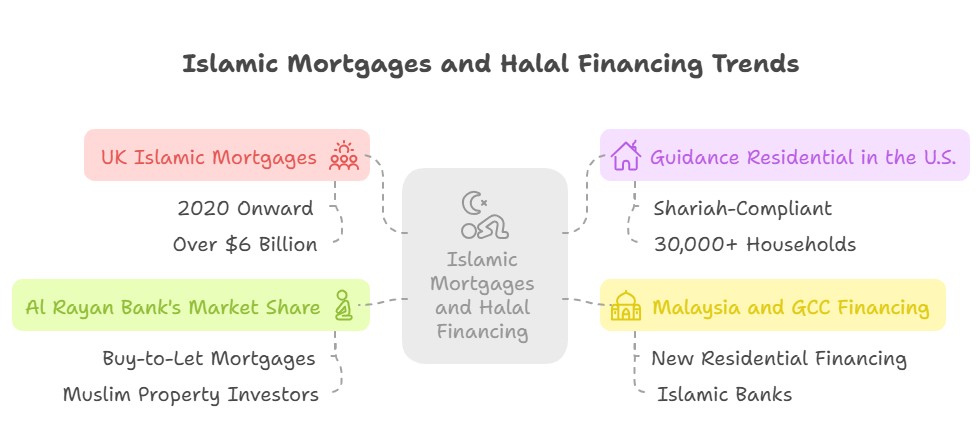

A Growing Global Trend

The expansion of Islamic finance across both Muslim-majority and non-Muslim countries reflects its broader appeal. Ethical investing, transparency, and shared-risk models are attracting a diverse range of homebuyers seeking alternatives to traditional systems.

Real-World Examples Across Countries

Countries like Malaysia have well-developed Islamic banking systems, while other regions are introducing innovative interest-free housing solutions adapted to local markets12.

{kind=link}

Why More People Are Choosing It

Growing awareness and research indicate that both individuals and organizations are increasingly choosing Islamic financing due to ethical considerations and alignment with values13.

- Religious alignment

- Ethical financial practices

- Transparency in agreements

- Avoidance of interest-based debt

Challenges and Areas for Improvement

Despite its growth, challenges remain, including lack of standardization and the complexity of some financial structures. Improving governance and transparency is essential for maintaining trust in the system14.

How It Fits into the Bigger Financial System

Sharia-compliant home financing is part of a broader Islamic banking ecosystem that includes savings, investments, and insurance solutions designed to align with ethical principles15.

Visual Overview of Islamic Banking

)

Key concepts of ethical finance including risk sharing, asset-backed transactions, and prohibition of interest

What This Means for Homebuyers in 2026

Homebuyers today have more financing options than ever before, allowing them to align their financial decisions with personal values. Choosing Sharia-compliant financing is not just about affordability but also about supporting a system grounded in fairness and responsibility16.

Final Thoughts

Sharia-compliant home financing represents a shift toward ethical and value-driven financial systems. By removing interest and focusing on transparency and shared responsibility, it offers a meaningful alternative for modern homebuyers.

As the system continues to evolve, it is becoming a significant part of the global housing market, appealing to those seeking both financial stability and ethical alignment.

Frequently Asked Questions

Question: What is Sharia-compliant home financing?

Answer: It is a method of purchasing property without interest, using ethical financial structures based on trade, leasing, or partnerships.

Question: Is Sharia-compliant financing more expensive than conventional loans?

Answer: Costs can vary, but payments are typically structured differently rather than being inherently more expensive, focusing on agreed profit instead of interest.

Question: Can non-Muslims use Sharia-compliant home financing?

Answer: Yes, these financing options are open to anyone interested in ethical, interest-free financial solutions.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.