)

Shariah Compliance in Property Loans: What It Means for Homebuyers in 2026

Key Takeaways

- Interest-Free Financing: Shariah-compliant loans avoid interest and rely on asset-based or partnership structures.

- Growing Global Trend: Demand is rising due to ethical finance awareness and strong ASEAN market growth.

- Multiple Financing Models: Murabahah, Ijarah, and Tawarruq offer different approaches to home financing.

- Transparency Matters: Clear disclosure is essential to avoid compliance risks and ensure trust.

- Accessible to All: These financing options are available to both Muslims and non-Muslims.

Introduction to Shariah-Compliant Property Loans

Shariah Compliance in Property Loans is quickly becoming one of the most talked-about topics in global finance—and for good reason. As more people seek ethical, transparent, and faith-aligned ways to finance their homes, Islamic finance is stepping into the spotlight in 2026.

From Southeast Asia to the U.S., banks, fintech startups, and regulators are reshaping how property loans work. But what exactly makes a property loan “Shariah-compliant”? And how is it different from a traditional mortgage?

Let’s unpack the trend, the mechanics, and what it means if you’re thinking about buying a home today.

What Is Shariah Compliance in Property Loans?

At its core, Shariah compliance in property loans means following Islamic law in financial transactions, particularly the prohibition of interest. Instead of lending money with interest, financial institutions structure deals around real assets and shared risk between parties1.

In practice, this means the bank typically purchases the property and then sells or leases it to the buyer at a profit, rather than charging interest on a loan. This structure fundamentally changes how pricing, risk, and transparency are handled.

Why Shariah-Compliant Financing Is Trending Now

The growing popularity of Shariah-compliant property loans is driven by a broader shift toward ethical finance, where consumers are more conscious of how financial products align with their values.

In ASEAN markets, strong regulatory support and innovation have accelerated adoption, making Islamic finance a key component of housing development strategies2.

At the same time, digital banking solutions are making these financing options more accessible, especially for younger buyers who expect seamless and transparent financial tools3.

How Shariah-Compliant Property Loans Work

There is no single model for Islamic home financing. Instead, several structures are used depending on the institution and region.

Murabahah (Cost-Plus Financing)

Under this model, the bank buys the property and sells it to the buyer at a pre-agreed profit margin, with payments made over time4.

Ijarah (Leasing Model)

In an Ijarah arrangement, the bank leases the property to the buyer, who gradually gains ownership through rental payments and eventual transfer5.

Tawarruq (Commodity-Based Financing)

This structure involves a series of commodity transactions to provide liquidity, though it is more complex and sometimes debated in terms of compliance.

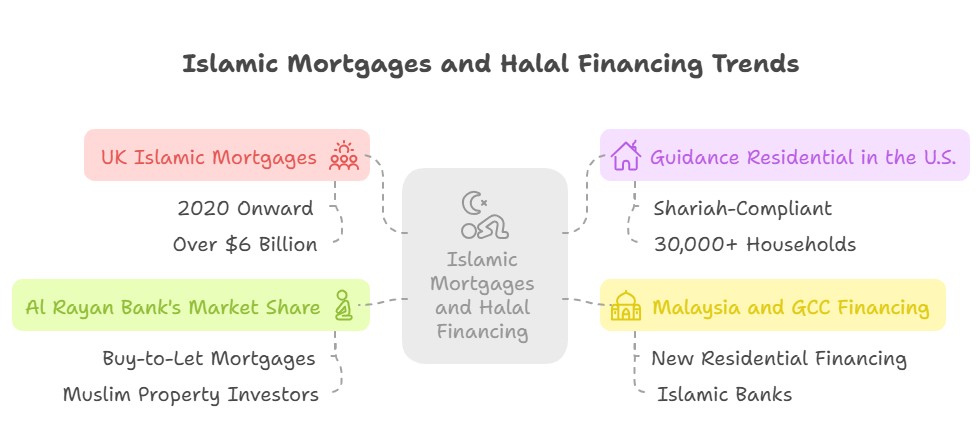

Visualizing the Concept

)

Financial structures emphasizing asset-backed transactions, shared risk, and ethical property financing principles

The Big Challenge: Shariah Non-Compliance Risk

Despite its benefits, Shariah-compliant financing is not without challenges. One key concern is ensuring that all aspects of a transaction genuinely adhere to Shariah principles, especially in complex models like Tawarruq6.

Issues such as unclear contract structures or misinterpretation of compliance rules can lead to risks for both financial institutions and buyers.

Transparency and proper disclosure are essential to reduce these risks and ensure that buyers fully understand what they are entering into7.

Affordable Housing and Financial Inclusion

Shariah-compliant financing is also playing a growing role in improving access to affordable housing, particularly in developing urban regions.

Its flexible structures and emphasis on fairness make it suitable for supporting lower-income buyers and promoting financial inclusion8.

The Global Expansion of Halal Real Estate

Shariah-compliant property financing is expanding beyond traditional markets, attracting global investors interested in ethical and diversified real estate portfolios9.

{kind=link}

Institutional products and funds are increasingly incorporating Shariah principles, signaling broader acceptance across international markets10.

{kind=link}

The Role of Technology in Modern Islamic Mortgages

Technology is transforming how Islamic mortgages are delivered, making them more user-friendly and accessible.

Digital platforms now allow buyers to manage accounts, track payments, and access financing tools in real time, improving overall transparency and efficiency.

What This Means for Property Buyers

For homebuyers in 2026, Shariah-compliant property loans offer an alternative approach rooted in ethical finance principles.

While these options provide transparency and fairness, they also require a deeper understanding of contract structures and financial mechanisms before making a decision.

Ultimately, choosing the right financing depends on individual priorities, financial goals, and comfort with the structure involved.

Final Thoughts: A Financial Shift Rooted in Values

Shariah Compliance in Property Loans represents more than just a financial alternative—it reflects a broader movement toward ethical and transparent financial systems.

As innovation continues and accessibility improves, these models are likely to play an increasingly important role in the global property market.

For buyers, understanding how these structures work is essential, because in this system, the method of financing is just as important as the outcome.

Frequently Asked Questions

Question: What makes a property loan Shariah-compliant?

Answer: A Shariah-compliant loan avoids interest and instead uses asset-based or partnership structures where profit is earned through trade or leasing.

Question: Are Shariah-compliant loans only for Muslims?

Answer: No, these financing options are open to anyone interested in ethical and transparent financial products.

Question: Is Islamic home financing more complicated than conventional loans?

Answer: It can be more complex due to different structures, but with proper understanding and guidance, it is manageable and increasingly user-friendly.

Disclaimer: The information is provided for general information only. BridgeProperties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.